Golden-Beacom College

Cola Wars Case Study

Team Members Contribution:

Abstract

This paper explores the strategies during cola wars, a long period of development and competition, between the top two carbonated soft drink companies in the world beverage market, Coca-Cola and Pepsi Co. Based on the decisions the two companies made, this paper conducts a situational analysis by looking at both the external and internal environments. The analysis is performed in four sections – human resources, strategic management, financial and marketing characteristics according to the article “Cola Wars Continue: Coke and Pepsi in 2010.” Throughout the analysis, this paper explains what decisions made in particular occasions and how the competition affects the development of not only Coca-Cola and Pepsi, but also the entire carbonated and non-carbonated drinks market in the worldwide.

Keywords: Coca-Cola, Pepsi, Human Resources, Strategic Management, Financial, Marketing Characteristics

Current Day Human Resources Analysis

Competition

For big companies or band names, companies don’t need to seek candidates by searching on Internet and advertising for open positions. Candidates will seek them out and submit application by various ways like internal referral, reaching out hiring manger through social network such as LinkedIn. Compared to small companies, it is very competitive for big companies to find competent candidates. So we believe companies like Coke needs to focus on strategies how to retain current employees and select best candidates through the candidate pool. Coke focuses on the acquisition and retention of highly skilled knowledgeable employees so that it can maintain it’s top positions in the market, while Pepsi focuses on employee development.

Both companies use traditional hiring process. Departments tell their need to HR department. And then recruitment is done on the requirement by the project. All candidates send their CV’s by post; they are then short listed and called. So those candidates then report at the company from where they are sent to the Human Resource Department for further interviews. But recently PEPSICO has devised a new way of recruitment i.e. Online Applications. They give Ads in leading newspaper and use some other mass media communication channels and then receive applications and CV’s online. In this way huge paper work is reduced.

Compensation

HR needs to keep the compensation fair and reasonable enough to keep current employees and to attract new hires. In a low demand job market, labor is more than industry needs. Company can lower the compensation to save cost but still have to make the compensation level attractive. When the job demand is high, companies would find harder to find best candidate, then they can raise the compensation level to attract new hires and keep current employees. I think the challenge for HR is whenever the demand of job market changes, HR always need to find a way to attract new employees, keep current employees at the same time to keep companies HR cost low.

In Pepsi, promotion is direct shift only to the next level from the current grade, the employee’s performance is evaluated and if his performance is above average he is given promotion. PEPSICO promotes only those candidates who are experienced and eligible for that particular vacancy. The company decides at the end of the financial year, according to its financial condition, whether increments should be given or not.

Legislation

Legislation is a key component throughout HR functions. HR needs to be fair in all HR related activities. Discrimination is strictly prohibited including race, gender, and religion. All hiring processes are required to comply with Federal and State laws. HR needs to be very careful when practicing their duties to prevent the company and him/herself being involved in any legal issues. HR also has responsibility to educate and supervise employees follow company policies.

Coke has the following statement regarding to legislation:” Coca-Cola does not support any legislation that discriminates, in our home state of Georgia or anywhere else. Coca-Cola values and celebrates diversity. We believe policies that would allow a business to refuse service to an individual based upon discrimination of any kind, does not only violate our Company’s core values, but would also negatively affect our consumers, customers, suppliers, bottling partners and associates. As a business, it is appropriate for us to help foster diversity, unity and respect among all people. We advocate for inclusion, equality and diversity through both our policies and practices. Coca-Cola does not condone intolerance or discrimination of any kind anywhere in the world.” Pepsi include this equal employment statement in their corporate governance.

Employee Relations

Besides the above issues HR needs to consider, employee relation is also a big topic that HR deals with. HR should lead the mid-year and year-end evaluation. Also they need to address various employee inquiries and issues. For example, when employees want to switch from one team to another within the company, HR is reached out and need to do the process of switch. Also, when people have personal issues need to take days off beyond company’s holiday, HR is involved at this time. HR also is responsible for company’s issues such as employee conflicts, attending management meeting and set salary and bonuses.

Based on Pepsi’s policy, the company is paying more attention to strengthen the relationship among employees by giving them equal opportunities to take advantage of the firm’s incentives, because no biasness among employees is practiced in the firm, which affects the good relations among employees. Coke transitioned their employee relations (ER) function to a centralized, shared services model in which nearly every employee issue is managed over the phone.

Strategy Analysis

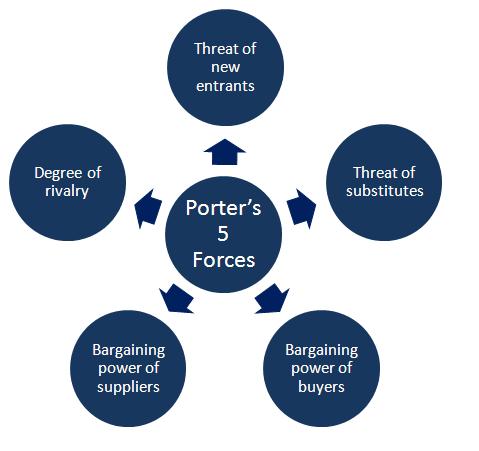

Porters Five Forces

Understanding the inner rivalry factors of an industry is the most customary practice since ages as it’s a door opener for potential vendors. Harvard Professor Michael Porter, made people understand a base model that models the impact of five powers on an industry. Examining the business’ basic structure is vital with these five strengths. The five focused influences that form the practice are: Threat of new entrants, Buyer power, Supplier power, Threat of substitutes and Degree of Rivalry.

These five strengths will help us understand how Pepsi Co and Coca Cola put their products in the market with the aim to survive the market rivalry, cut throat competition and with increased productivity and profitability.

Threat of New Entrants

There is always a threat and pressure in the industry when there is a new entrant in the market. It means new fulfilment, bigger market chunk, that ultimately increases your costs, and the important speculating rates. The threat of another segment is remarkably low in soda sector. Fundamentally, Coca Cola was the undoubted leader in the market, until the new entrant Pepsi’s huge entry shook the industry and Coke’s remarkable offers offered. Today, Cola-Wars between these two rivals Coke and Pepsi are leading to the point, that the new entrant threat is minimal in this sector.

In various countries, the marketing, production, distribution and sales are according to their countries’ specific political control. There are various environmental and safety laws that are to be adhered for all existing and new entrants that makes it difficult to enter that countries’ market.

The customer brand loyalty being high, the fences to such new entrants in carbonated soda sectors are pretty much high. The rivalry risk has very less weightage in the drinks business because of the shoppers’ low expense. The various barriers such as high investments costs for setting up a production plant and packaging, competition for storage space, raising costs of trademarks violation make this compel and low for such business model.

The most basics are marketing and advertisement in CSD industry which requires huge chunks of cash. In 2000, Pepsi, Coke and their bottling units contributed approximately $2.57 billion. In 2000, the average advertisement expenditure per point of market share was $8.4 million. This makes it an absolute no-no situation for new entrant to combat with the current competition and grow, simultaneously.

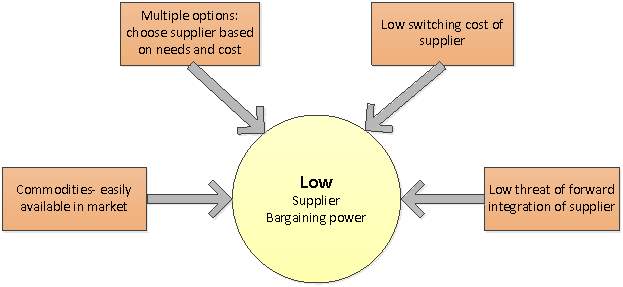

Buyer Power

Buying power is one of the most important aspect. Buyers are solid if they have capacity to fulfil needs. The industry has a huge to offer but it is difficult to get the pie of the marker share. The main buyers for the Carbonated Soft Drink (CSD) industry are fast food fountain, vending machines, food stores, convenient stores, restaurants, college canteens and gas stations. These have different profitability ratios, which displays the bargaining power of the buyer to pay different prices based on their power to negotiate. An average American consumes 56 gallons of soda a year. Costing just under $2, makes it affordable for many as individuals.

In we look at the fast food fountain division, the bargaining power of buyer is high since there is a mass consumption and productivity is the smallest chunk. In Vending machine division, the buyer has no power- this channel serves the clients specifically to their needs. The store section is divided and has no dealing power as well. On basis of this, for this situation, buyer’s bargaining power is weak, particularly in USA. But in countries like China and India, buyers have great negotiating powers as buyers’ market is not as shared as American market.

Moreover, Coke and Pepsi had a franchisee agreement that hampered the bargaining power of bottlers and enormous fast-food eateries and buy their acquisition simultaneously. Coke’s Master Bottler Contract permitted the privilege to Coke to decide focus cost and different conditions of offers while Pepsi’s Master Bottler Contract permitted Pepsi the privilege to compel its bottlers to buy crude materials from Pepsi at costs and on terms and conditions measured by Pepsi. Pepsi then added Pizza Hut in 1978, KFC in 1986 and Taco Bell in 1986 while Coke only had managed Burger King and McDonald’s.

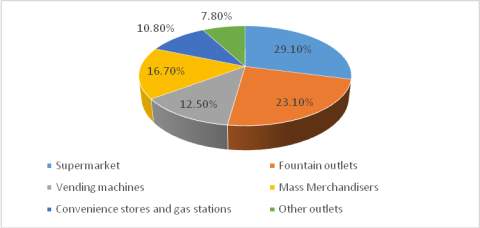

As indicated by Beverage Digest Fact Book, the distribution of CSDs in the United States occurred through general stores (29.1%), fountain outlets (23.1%), vending machines (12.5%), mass merchandisers (16.7%), accommodation stores and service stations (10.8%), and different outlets (7.8%). Small markets and medication tie-ups made up most of the last class. The offers of CSDs represented 4 percent of aggregate store deals in the U.S. Bottlers battled for rack storage space to make item visibility and customer appeal; and thus, rivalry for attractive rack storage space in retail industry that gave buyers some power to deal with the providers.

Supplier Power

The providers do make maximum profits by charging higher costs or compelling quality to the business. In CSD industry, the bargaining power of supplier is often low as there are many providers associated with the business. The industry often requires huge raw materials to make assorted flavors, caffeine and added substances, sweeteners and water. These are the fundamental goods that are accessible effortlessly. The makers have no power over the pricing and thus providers in this segment are powerless. As Coke and Pepsi have a huge chunk of the market share in the CSD business, providers of the such crude items have no or less dealing power.

All these basic ingredients are fundamental products that are effectively and easily available to the producers. So, in this case the makers cost of shifting is low and so they can easily without much of a hassle can switch to alternate providers. In this case, Coke and Pepsi bottlers offered “direct store door” (DSD) conveyance, a plan wherein the conveyance salesmen dealt with the CSD mark in stores by securing rack storage space, stacking CSD items, positioning the brand’s trademarked name, and setting up purpose of-procurement or end-of-path cabinets. This establishes because of the rivalry in the bottlers; bottlers are putting forth more esteem additional items to their administration to keep the agreement with the Coke and Pepsi.

As per case the dominant part of U.S. CSDs were bundled in metal cans (57%), with plastic bottles (41%) and glass bottles (2%) and Coke and Pepsi consulted for the benefit of their packaging systems, and were one of the metal can industry’s biggest clients, which gave them negotiating powers over providers.

Similarly, for the most part the suppliers group can threaten the makers to synchronize forward into the business. However, being low on risk in this industry, producers of the soft drinks need huge manufacturing plants, packaging system, best retire space and strong distribution network. Supplier in CSD industry can’t manage the cost of such sort of settled framework and system. Hence, minimal risk.

Threat of Substitutes

In the five-force model, the threat of substitutes means goods and services that perform similar functions. A substitute product is another product from the industry that gives similar benefits to user as the product is produced by the companies in same segment. The hovering threat of substitution in the segment impacts heavily on the competition within the firms and influences those firms’ capability to achieve profitability.

The availability to end consumers is huge in CSD industry, as they have large numbers of substitutes like water, beer, wine, coffee, milk, tea, juices, low calorie drinks etc., available. The companies diversify business by offering substitutes to armor themselves from competition. Ex: Pepsi produces Mug Root Beer (1.5% market share), Slice fruit juice (0.4% ) and Tropicana fresh juices. Coke produces Barq’s and Diet Barq’s (0.5%), Minute Maid brands producing fresh fruit juices (1.6 %). By diversifying, the market share of the company raised to greater heights. Coke recorded a high of 43%, after diversifying from 33.4%, when it was restricted to only Coca-Cola. On the other hand, Pepsi rose from 20% to 31% whereas, Cadbury rose from 4.7% to 14.5%.

The soft drink industry has countered threat of substitute via massive advertising, brand equity, and making the products easily accessible to consumers, which most substitutes cannot bout. The poor industry product performance leads to lower threat of substitution. Also, tremendous brand loyalty of customers minimizes the threat of substitutes, but in today’s health conscious lifestyle of people who are well aware of issues such as obesity, can increases demand of healthy beverages from the healthier drinks every year and thus could increase the threat of healthier substitutes to the Cola Giants.

As it is very easy to switch between products and people, the switch over cost is low, especially when youth is looking for diet and healthy drinking options with no added caffeine. Hence, in this case the threat of substitute to CSD industry is on the higher end.

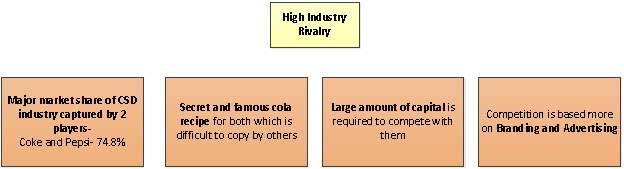

Competitive rivalry among established firms: In today’s competitive market, the rivalry being super strong, the competitors are trying their best to hit rock-bottom in profits and market share from each other. The non-alcoholic beverage industry is hugely dominated by Coke and Pepsi having majority of the market share compared to other players having very less sizable chunk. Remarkably, both Pepsi Co and Coca Cola primarily are competing through distinction in their branding than on pricing, which always permitted higher profits in their businesses despite of intense competition. They also expanded business internationally for growth, but major aspect is that the pricing war was never experienced in their expansion.

There is a global scope of competition in this industry, in which Coke and Pepsi are selling their products in approximately 250 countries. These rivals are striving hard to increase and differentiate their product portfolio, spending huge piles of money on promotional and advertising strategies just to retain the market share. In the entire history of CSD, non-alcoholic beverage industry, Coke and Pepsi had a high degree of rivalry and always fought for a bigger market share and did survive in the intra-rivalry of the industry.

Financial Analysis

Return on Equity (ROE) Analysis

According to My Accounting Course (2017), ROE is a profitability ratio tool that is used to measure a company’s ability to generate profits for its shareholders investments. Potential investors are often very cautious and wanted to make sure that their money are invested in the most profitable ways and in a firm that is reputable and have a good track records of generating lots of returns in profits for their investments. For example, a return on 1 means the common stockholders will receive 1 dollar of net profit for every dollar they invested in a company. This is a very crucial measurement for potential investors because it helps them to gage how efficiently a firm utilizes their investments to generate net income. Furthermore, ROE is also serves to convey how effective the firm’s management is at handling equity financing to grow the company and to fund its operations. ROE also reveals how well corporate strategies perform. Furthermore, ROE is a very good measuring tool for comparing profitability among companies.

Below is the analysis comparing the Return on Equity (ROE) between Coca-Cola Company and PepsiCo, Inc. for the time period between 1980 through 2009 base on Exhibit 3a Financial Data for Coca-Cola and PepsiCo ($ millions.)

According to (Yoffie & Renee, 2011), both Coca-Cola Company and PepsiCo, Inc. were tied at 20% for their ROE. In 1985, both Coca-Cola Company and PepsiCo, Inc. had increased ROE but at different rates. Coca-Cola Company’s ROE increased from 20% to 24% while PepsiCo, Inc.’s ROE jumped from 20% to 30%. In 1990, Coca-Cola Company’s ROE climb to 36% while PepsiCo, Inc.’s ROE declined to 22%. In 1995, Coca-Cola Company’s ROE continued to climb to 55.4% while PepsiCo, Inc.’s ROE dropped to an even lower 19%. In 2000, Coca-Cola Company’s ROE had a stiff dropped from 55.4% to 23.4% as compare to PepsiCo, Inc.’s ROE increased from 19.4% to 30.1%. In 2005, Coca-Cola Company’s ROE rose back up to 29.9% from 23.4% at the same time PepsiCo, Inc.’s ROE dipped to 28.6%. In 2007, Coca-Cola Company’s ROE lower to 27.5% from 29.8% as PepsiCo, Inc.’s ROE increased from 28.6% to 32.8%. In 2008, Coca-Cola Company rose .9% from 27.5% and made it 28.4% meanwhile PepsiCo, Inc.’s ROE had a 9.7% increased from 32.8% boosted it to 42.5%. In 2009, both competitors’ ROE had a decrease. Coca-Cola Company’s ROE went back down to 27.5% from 28.4%; PepsiCo, Inc.’s ROE decreased from 42.5% to 35.4%. (Coke & Pepsi financial date Exhibit 3a – ROE).

Coca-Cola Company and PepsiCo, Inc. are two soft drink industry giants whom has been rivalries in the war to dominate the beverage market both domestically and internationally for decades and will continue for years to come. Based on the analysis above, both Coca-Cola Company and PepsiCo, Inc. had their ups and downs for the time durations between 1980 through 2009. There are so many criteria that could affect a company’s annual ROE. Advertising strategies, economic depressions, personal preferences, prices, bottle designs, and locations among other factors could either mildly or greatly influence sale results.

Operating Profit Analysis

According to The Strategic CFO (2017), operating profit margin ratio can be calculated by using Operating profit margin = Operating income ÷ Total revenue or EBIT ÷Total revenue. Operating profit margin ratio reveals how much profit a company earns after all its expenditures such as raw materials, wages, overheads, among other costs have been deducted. It is shown as a percentage of sales and is utilized to indicate how efficiently a company controlling the costs and expenses associated with its business operations. Moreover, operating profit margin simply means the return achieved from standard operations and excludes one time or unique transactions. The term operating profit margin ratio also encompass operating margin, operating income margin, operating income margin, or return on sales (ROS).

Below is the analysis comparing Coca-Cola Company Beverages, North America operating profit versus Coca-Cola Beverage, International operating profit for the time period between 1980 through 2009 base on Exhibit 3a Financial Data for Coca-Cola and PepsiCo ($ millions.)

According to (Yoffie & Renee, 2011), In 1980, Coca-Cola Company Beverages, North America operating profit was at 11.1% while Coca-Cola Company Beverages, International operating profit was at 21% 1985 – 1990 both Coca-Cola Company Beverages, North America operating profit and Coca-Cola Company Beverages, International operating profit had increases. North America was at 11.6% and 16.5% as compared to International at 22.9% and 29.4% consecutively. In 1995, both Coca-Cola Company Beverages, North America operating profit and Coca-Cola Company Beverages, International operating profit suffer minor decreased. North America was at 15.5% and International was at 29.1%. In 2000, Coca-Cola Company Beverages, North America operating profit had a slight increase to 17.9% while Coca-Cola Company Beverages; International continued to drop to 27.1%. In 2005, both Coca-Cola Company Beverages, North America operating profit and Coca-Cola Company Beverages, International operating profit jumped to their peaks with North America at 23.3% and International at 35.4%. In 2007, both Coca-Cola Company Beverages, North America operating profit and Coca-Cola Company Beverages, International operating profit went back down slightly with North America at 21.6% and International at 33.2%. In 2008, Coca-Cola Company Beverages, North America operating profit slid to 19.1% but International climbed back up to 35.2%. In 2009, Coca-Cola Company Beverages, North America operating profit went up to 20.5% but International went down to 34.6%. (Coke & Pepsi financial date Exhibit 3a – Cokes Operating Profit).

Coca-Cola beverages are abundant at its best. Almost everywhere there is a beverage vendor or a vending machine there will be Coca-Cola available to be purchased. It is obvious that Coca-Cola Company Beverages, International covers more geographic areas and therefore generates more sales than North America. However, based on exhibit 3a, North America alone sales nearly half the volume of beverages comparing to its international counterpart.

Net Profit Analysis

According to investing answers (2017), net profit is a company’s total revenue minus all taxes, interest, operating expenses, and preferred stock dividends (but not common stock dividends.) The formula to calculate net profit margin is: (Total revenue – Total expenses)/Total Revenue = Net Profit/Total Revenue = Net Profit Margin. Investors monitor net profit margin closely because it shows how effectively a company is at converting revenue into profits for its shareholders. Investors will closely examine declining net profit in a company over a period of time. It’s will cause panic to shareholders and the blaming will range from poor customer experience to decreasing sales to not enough expense management.

Below is the analysis comparing the net profit between Coca-Cola Company and PepsiCo, Inc. for the time period between 1980 through 2009 base on Exhibit 3a Financial Data for Coca-Cola and PepsiCo ($ millions.)

According to (Yoffie & Renee, 2011), In 1980, Coca-Cola Company and PepsiCo, Inc. had a 7.7% net profit as compared to PepsiCo, Inc. at 4.4%. 1985 – 1995, both Coca-Cola Company and PepsiCo, Inc. had consecutive increased net profits. Coca-Cola Company was at 12.3% in 1985, 13.5% in 1990, and 16.5% in 1995 while PepsiCo, Inc. was at 5.6%, 6.2% and 7.5% respectively. In 2000, Coca-Cola Company’s net profit dropped to 10.6% as compare to PepsiCo, Inc. increased to 10.7%. In 2005, both Coca-Cola Company and PepsiCo, Inc.’s net profit went back up with Coca-Cola Company at 21.1% and PepsiCo Inc. at 12.5%. In 2007, Coca-Cola Company’s net profits lower to 20.7% as Inc. increased to 14.3%. In 2008, both Coca-Cola Company declined to 18.2% and PepsiCo, Inc. dropped to 11.9%. In 2009, both rivals had an increase. Coca-Cola Company was at 22%; PepsiCo, Inc. was at 13.8%. (Coke & Pepsi financial date Exhibit 3a – Coke and Pepsi Net Profit)

Net profit is a very important tool that all investors and shareholders use to monitor their potential investment companies’ abilities to generate revenue. Furthermore, investors to compare companies within the same industry in a process called “margin analysis” frequently use net profit. The major key in understanding net profit is not how much money a company could make in a given period of time as a company’s income statement covers a lot of non-cash expenses such as amortization and depreciation. To learn how well a company generates cash, one must look into the company’s cash flow statement.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cola Wars – Financial Analysis – Cokes Operating Profit | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exhibit 3a Financial Data For Coca-Cola and PepsiCo ($ millions) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1975 | 1980 | 1985 | 1990 | 1995 | 2000 | 2005 | 2007 | 2008 | 2009 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coca-Cola Company | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Beverages, North America: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North America Operating Profit | 165 | 216 | 406 | 855 | 1,409 | 1,556 | 1,693 | 1,581 | 1,696 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | – | 1,486 | 1,865 | 2,461 | 5,513 | 7,870 | 6,676 | 7,836 | 8,280 | 8,271 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating profits/sales | – | 11.1% | 11.6% | 16.5% | 15.5% | 17.9% | 23.3% | 21.6% | 19.1% | 20.5% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Beverages, International: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| International Operating Profit | 493 | 613 | 1,801 | 3,655 | 3,411 | 5,786 | 6,898 | 7,959 | 7,692 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | – | 2,349 | 2,677 | 6,125 | 12,559 | 12,588 | 16,345 | 20,778 | 22,611 | 22,231 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating profits/sales | – | 21.0% | 22.9% | 29.4% | 29.1% | 27.1% | 35.4% | 33.2% | 35.2% | 34.6% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cola Wars – Financial Analysis – Coke and Pepsi Net Profit | ||||||||||

| Exhibit 3a Financial Data For Coca-Cola and PepsiCo ($ millions) | ||||||||||

| 1975 | 1980 | 1985 | 1990 | 1995 | 2000 | 2005 | 2007 | 2008 | 2009 | |

| Coca-Cola Company | ||||||||||

| Consolidated: | ||||||||||

| Coke Consolidated Net Profit | 250 | 422 | 723 | 1,382 | 2,991 | 2,169 | 4,875 | 5,973 | 5,814 | 6,818 |

| Sales | 2,773 | 5,475 | 5,879 | 10,236 | 18,127 | 20,458 | 23,104 | 28,857 | 31,944 | 30,990 |

| Net profit/sales | 9.0% | 7.7% | 12.3% | 13.5% | 16.5% | 10.6% | 21.1% | 20.7% | 18.2% | 22.0% |

| PepsiCo, Inc. | ||||||||||

| Consolidated: | ||||||||||

| Pepsi Consolidated Net Profit | 125 | 263 | 425 | 1,086 | 1,430 | 2,187 | 4,070 | 5,645 | 5,147 | 5,966 |

| Sales | 2,709 | 5,975 | 7,585 | 17,515 | 19,067 | 20,438 | 32,562 | 39,474 | 43,251 | 43,232 |

| Net profit/sales | 4.6% | 4.4% | 5.6% | 6.2% | 7.5% | 10.7% | 12.5% | 14.3% | 11.9% | 13.8% |

Marketing Analysis

Product

In 1866, Coca-Cola was invented by John Pemberton, who sold it as a “potion for mental and physical disorders” in soda fountains in a drug store. In 1893, Pepsi was initially formulated by Caleb Bradham, who is a pharmacist in North Carolina.

Coca-Cola and Pepsi kept selling their initial cola brands for decades, until they finally decided to make some changes and innovation by investigating the new flavors and changing the design. In 1950, Pepsi introduced a 26-oz bottle to target family consumption. At the same time, Pepsi’s growth followed the postwar market growth in the US. Diet Coke was released to the public around 1982 and it had become the top low-calorie drink all over the world within two years, entering the market and attracting the consumers’ attention successfully. In 1985, Coca-Cola pioneered to change the formula with its “New Coke”. Although most of the consumers accept the new flavor, they still have a deep emotional attachment to the original flavor. At last, the company had to let the old drink return to the market and name it as Coca-Cola Classic.

Following the first step, Coca-Cola launched Fanta, Sprite and the low-calorie cola Tab within the next decade. Later in 1990s, more and more new beverages joined this family, including Powerade sports drinks and Oasis fruit drinks. Also some brands were acquired by Coca-Cola, like Barq’s root beer in the US, Limca, Mazza and Thumps Up in India, Inca Kola in Peru and so on (http://www.coca-cola.co.uk/stories/our-story-1990-1999–new-drinks–new-characters).

Pepsi also started to experiment on new flavors since then and introduced 13 products. In 1982, Pepsi Free and Diet Pepsi Free, the first major brand caffeine-free colas, are released to the public. After six years, Pepsi Wild Cherry was introduced as a cherry flavored cola. Besides, Pepsi also countered Lemon-Lime Slice, Mountain Dew, Teem, Diet Pepsi and so on in market to compete with Coke. By the late 1980s, Coke and Pepsi each offered more than 10 major brands and 17 or more container types (Yoffie & Kim, 2011).

In the first decade of 20th century, both Coca-Cola and Pepsi made efforts to change their sweeteners. Pepsi used high-fructose corn syrup to replace natural sugar for Pepsi Throwback and Mountain Dew Throwback. Coke and Pepsi developed their own Stevia-based sweetener, and followed by the introduction of the new products, including Coke’s Sprite Green and Pepsi’s reduced-calorie Trop 50 (orange juice).

At the same time, Coke and Pepsi started to involve “non-carb” market, which including juices and juice drinks, sports drinks, energy drinks and tea-based drinks. Between 2004 and 2007, Pepsi was very aggressive on expanding in non-carb market, releasing non-carbs 77% of its new products, comparing with Coke’s 56%. After 2007, Coke utilized acquisition to develop the market. By 2009, Coke had 32% of the US non-carbs market share compared to Pepsi’s 32%.

Price

Both Coca-Cola and Pepsi tried hard to beat each other during the long-period cola wars with price superiority. At the very beginning, Pepsi was struggled since the leadership of Coca-Cola in the carbon soft drink market, and it declared bankruptcy in 1923 and again in 1932. The main reason of its business taking a turn for the better was that Pepsi started to sell its 12-oz bottle by 5 cents, which is the same price that Coke charged for a 6.5-oz bottle, during the Great Depression (Yoffie & Kim, 2011).

By 1970, Pepsi sold their concentrate to bottlers as a 20% lower price than Coke did, in order to remain the larger number of their bottlers, and it succeed. In the early 1970s, Pepsi changed its strategy and increased concentrate price to equal with Coca-Cola. Later in 1978, Coke had its bottlers to approve a new contract to gain more flexibility in pricing concentrate and syrups, by adjusting the price to reflect any cost changes of the ingredient and changing and supplying unsweetened concentrate to bottlers who preferred to purchase other sweeteners in the market (Pendergrast, 1993). Since then, Coke announced a concentrate price increase, and Pepsi followed to have a 15% price increase.

From both of Coca-Cola and Pepsi sides, the price is based on product value, market and geographic segment. Each of the sub-brand of Coke and Pepsi has different pricing strategy, but they are all according to competitor pricing (Bhasin, 2017). They have to maintain affordable price points to appeal to their vast middle class market since they have a direct competition relationship with each other, regardless of their leadership status in the market. In other words, the pricing relies on each other’s price, and it would not increase nor decrease too much within a period. Otherwise a number of consumers may shift to the other brand if the price raised a lot, or may get the impression that the quality has become worse. In the long term, the actions of Coca-Cola and Pepsi’s narrowing the price gap can keep the cost low for consumers.

Place

The original carbonated soft drinks of both Coca-Cola and Pepsi were sold in the regular soda fountain in drug stores at the very beginning. Since then, they both built a large franchise bottling system. Begin in 1942, Coca-Cola started to sell the beverages to the military or to the retailers that served soldiers by exempting wartime sugar rationing. Thanks to this strategy, Coke bottling plants followed the US troops. During the war, the US government set up 64 such plants overseas, which is conducive to Coke’s postwar market shares in most of European and Asian countries. In the 1940s, Pepsi had to rely on the local small bottlers to compete with the established Coke franchisees and gain the market share little by little, and it succeeded to become the second largest carbonated soft drink brand, followed by Royal Crown and Dr. Pepper.

In the late 1980s, Coke created its own bottler company Coca-Cola Enterprise (CCE), and CCE consolidated small territories into larger regions, renegotiated contracts with suppliers and retailers. On the other hand, Pepsi acquired several bottling firms. The consolidation of bottler significantly made the concentrate producers dependent on Coke and Pepsi bottling networks to distribute their products and gained more control for Coke and Pepsi to manage their distribution channel. Starting in the late 1990s, the possibility of consumption pattern shift drove Coke and Pepsi tried to work on innovation and marketing. For Coca-Cola, it released a new freestyle soda machine in 2009, which creates different kinds of custom beverages to replace a regular soda fountain in some places.

Coca-Cola and Pepsi also expanded their international market in a long period. While the US remained as the largest market for carbonated soft drinks, they accounted for a third of global consumption, followed by Mexico, Puerto Rico, and Argentina (Yoffie & Kim, 2011). Additionally, the markets in Asia and Eastern European developed much faster than they did before. Among them, especially China and India formed an impressive large market. Served in more than 200 countries, Coca-Cola derived about 80% of its sales from international market (Williams, 2009). For Pepsi, it relied on the main US market for almost half of its total sales. By the early 2000s, Pepsi focused on emerging markets and it had its top carbonated soft drink markets in Asia, Middle East and Africa.

Generally, Coca-Cola and Pepsi have their products in wholesales, supermarket and other retailers, restaurants, automated teller machines, gas stations all over the world. According to Beverage Digest Fact Book 2010, the main distribution of carbonated soft drinks in the United States is in Table 1. The main three channels in which products reach the market: direct store delivery (DSD), customer warehouse, and third-party distributor networks. Product characteristics, customer needs and local trade practices are the base of how Pepsi chooses the relevant distribution (Bailey, 2014).

Table 1. The Distribution of Carbonated Soft Drinks in the U.S. (2009)

Promotion

During 1920s and 1930s, Coca-Cola first placed open-top coolers in grocery stores and other retail channels, and it advertised “lifestyle” for the time, to emphasize the role of Coke in consumer’s life. In 1963, Pepsi launched its “Pepsi Generation” marketing campaign and targeted the young and “young at heart”. The campaign helped Pepsi narrow Coke’s lead to a 2-to-1 margin. In the late 1950s, Coke started to use advertising messages like “American’s Preferred Taste” and “No Wonder Coke Refreshes Best” to state its advantage over its competitor. In 1974, Pepsi launched the “Pepsi Challenge” in Dallas, Texas. Coke was the dominant brand in the city, and Pepsi ran a series of blind taste tests to try to indicate that consumers preferred Pepsi to Coke actually. After the success in Dallas, Pepsi rolled out the campaign nationwide.

Facing the decrease sales of carbonated soft drinks trend in 2000s, Coke placed a greater emphasis on promoting its brand, spending $230 million in advertisement of its drinks. It also spent a lot on sponsorship and global marketing, such as $600 million for the world cup in 2010 (Bauerlein & Stewart, 2010). On the other hand, Pepsi redesigned its logo in 2008 with a three-year rebranding plan and tried to rebuild its image. Since market survey indicates that more consumers preferred Coke to Pepsi as their favorite carbonated soft drink, Pepsi focused on remodel its overall portfolio as a snack and beverage company.

In 2016, Coke announced that all of Coke Trademark brands united in one global creative campaign “Taste the Feeling”. It brings the new idea that drinking any Coca-Cola is a simple pleasure that makes every moment more special. To make it successful, four agencies, Mercado-McCann, Santo, Sra. Rushmore and Oglivy & Mather, produced an initial round of 10 TV commercials, digital, print, out-of-home and shopper materials. Six additional shops will contribute creative as the campaign evolves (Moye, 2016). For Pepsi, it started to market specially designed emoji cans and bottles to more than 100 global markets in 2016, including the U.S, Russia, Canada and Thailand, which are called “PepsiMojis.” Pepsi supported the program with both digital and traditional advertising. It also has plans to extend the emojis beyond packaging. As Women’s Wear Daily recently reported, Pepsi has teamed up with fashion designer Jeremy Scott on a collection of PepsiMoji-inspired sunglasses (Schultz & Wohl, 2016).

Conclusion

In 1980s, Coca Cola and Pepsi began their mutually targeted television advertisements campaign which later became known as Cola Wars. Based on reviewing and analyzing their products, marketing strategies, human resources and finances, we can conclude the following:

Both companies achieved average annual growth of 10% due to increased consumption in the US and worldwide between 1975 and 1995. The overall consumption of CSD dropped for two consecutive years and that resulted in decrease of the sales and therefore decrease in the profit in late 90s. They were trying to bring the business back releasing new products – derivative of the regular coke. Coke and Pepsi-Cola need to focus on their international sales. Both the companies must deal with the fact that the US is engaged in anti – terrorism activities which has a substantial impact on their sales in the Arabic states. They tried to adapt the product to the respective cultural specificities. Diversification should be more to minimize risk in case the CSD business is slowing down for a longer time for Coca Cola and Pepsi. This means that they should shift some investments in assorted products and while Pepsi is doing exactly that Coke is only focusing on the beverages. Both the companies should have in mind the low – price produces which hold a market share of 20 % worldwide if they want to keep and increase their sales. Coca Cola and Pepsi should strengthen their brand image and keep their original brand architecture but allow local markets to develop their own to adapt more quickly. Recent surveys show that consumers are more willing to buy a product or a variation of a product that they are familiar with – for example coke with assorted flavors. Coke and Pepsi were, are and will always be one of the biggest CSD companies in the world. They will always strive hard to get their bigger chunk of market share with consumers’ needs in mind.

References

Bailey, S. (2014, Dec 12). PepsiCo’s three-channel distribution network. Retrieved April 26, 2017, from http://marketrealist.com/2014/12/pepsicos-three-channel-distribution-network

Bauerlein, V. & Stewart, M. R. (2010, June 29). Coke Poured the Pressure on in World Cup of Marketing.

Beverage Digest Fact Book 2010. (2010).

Bhasin, H. (2017, April 15). Marketing mix of Coca Cola – Coca cola marketing mix. Retrieved April 26, 2017, from http://www.marketing91.com/marketing-mix-coca-cola

Coca-Cola Stories. (n.d.) In Coca-Cola. Retrieved April 26, 2017, from http://www.coca-cola.co.uk/stories/our-story-1990-1999–new-drinks–new-characters

Kokemuller, N. (n.d.). What Is the Marketing Mix of Coca Cola? Retrieved April 26, 2017, from http://yourbusiness.azcentral.com/marketing-mix-coca-cola-12969.html

Lu, L. & Tiwana, S. (2015, May 17). The Coca-Cola Company’s distribution strategy. Retrieved April 26, 2017, from https://mpk732.wordpress.com/2015/05/17/the-coca-cola-companys-distribution-strategy

Moye, J. (2016, January 19). ‘One Brand’ Strategy, New Global Campaign Unite Coca-Cola Trademark. Retrieved April 27, 2017 from http://www.coca-colacompany.com/stories/taste-the-feeling-launch

Pendergrast, M. (1993). For God, Country and Coca-Cola.

Schultz, E.J. & Wohl, J. (2016, February 19). Pepsi Preps Global Emoji Can and Bottle Campaign. Retrieved April 27, 2017, from http://adage.com/article/cmo-strategy/pepsi-preps-global-emoji-bottle-campaign/302748

Williams, C. (2009, August 17). Coke’s Fortunes are Set to Pop. Retrieved April 26, 2017, from http://www.barrons.com/articles/SB125029831086233597

Yoffie, B. D. & Kim, R. (2011, May 26). Cola Wars Continue: Coke and Pepsi in 2010

Yoffie, David B., and Renee Kim. “Cola Wars Continue: Coke and Pepsi in 2010.” Harvard Business School Case 711-462, December 2010. (Revised May 2011.)

Return on Equity Ratio | Analysis | Formula | Example. (n.d.).

Retrieved April 28, 2017, from http://www.myaccountingcourse.com/financial-ratios/return-on-equity

Operating Profit Margin Ratio • The Strategic CFO. (2017, March 16).

Retrieved April 28, 2017, from https://strategiccfo.com/operating-profit-margin-ratio/

Net Profit Margin Analysis • The Strategic CFO. (2017, February 13).

Retrieved April 28, 2017, from https://strategiccfo.com/net-profit-margin-analysis/

Net Profit Margin. (n.d.).

Retrieved April 28, 2017, from http://www.investinganswers.com/financial-dictionary/financial-statement-analysis/net-profit-margin-2233

The Wall Street Journal & Breaking News. (n.d.).

Business, Financial and Economic News, World News and Video. Pepsi Scores One on Coke, GainsSponsorship Rights to the NFL – WSJ. Retrieved from http://www.wsj.com/articles/SB1017339280423008000

You have to be 100% sure of the quality of your product to give a money-back guarantee. This describes us perfectly. Make sure that this guarantee is totally transparent.

Read moreEach paper is composed from scratch, according to your instructions. It is then checked by our plagiarism-detection software. There is no gap where plagiarism could squeeze in.

Read moreThanks to our free revisions, there is no way for you to be unsatisfied. We will work on your paper until you are completely happy with the result.

Read moreYour email is safe, as we store it according to international data protection rules. Your bank details are secure, as we use only reliable payment systems.

Read moreBy sending us your money, you buy the service we provide. Check out our terms and conditions if you prefer business talks to be laid out in official language.

Read more